(BY SHAYON SENGUPTA)

This essay assumes some familiarity with MEV. See Tokenizing MEV for a primer on Miner Extractable Value and the market structure between searchers and block producers.

Miner Extractable Value (MEV) is fundamental to permissionless distributed systems and cannot be eliminated.

The market structure for MEV is dynamic and complex, but the actors that profit from them in proof-of-work (PoW) networks—such as Ethereum 1.0—have exclusively been miners and searchers.

MEV historically has been a balance between these two entities. For any given opportunity, searchers perform the tasks of technically optimizing a set of transactions and evaluating the game theory of sharing a percentage of potential profits with the miner that chooses to include their attempt amidst several competitors. Note that both the profits paid to the miner and the profits extracted by the searcher are classified as MEV.

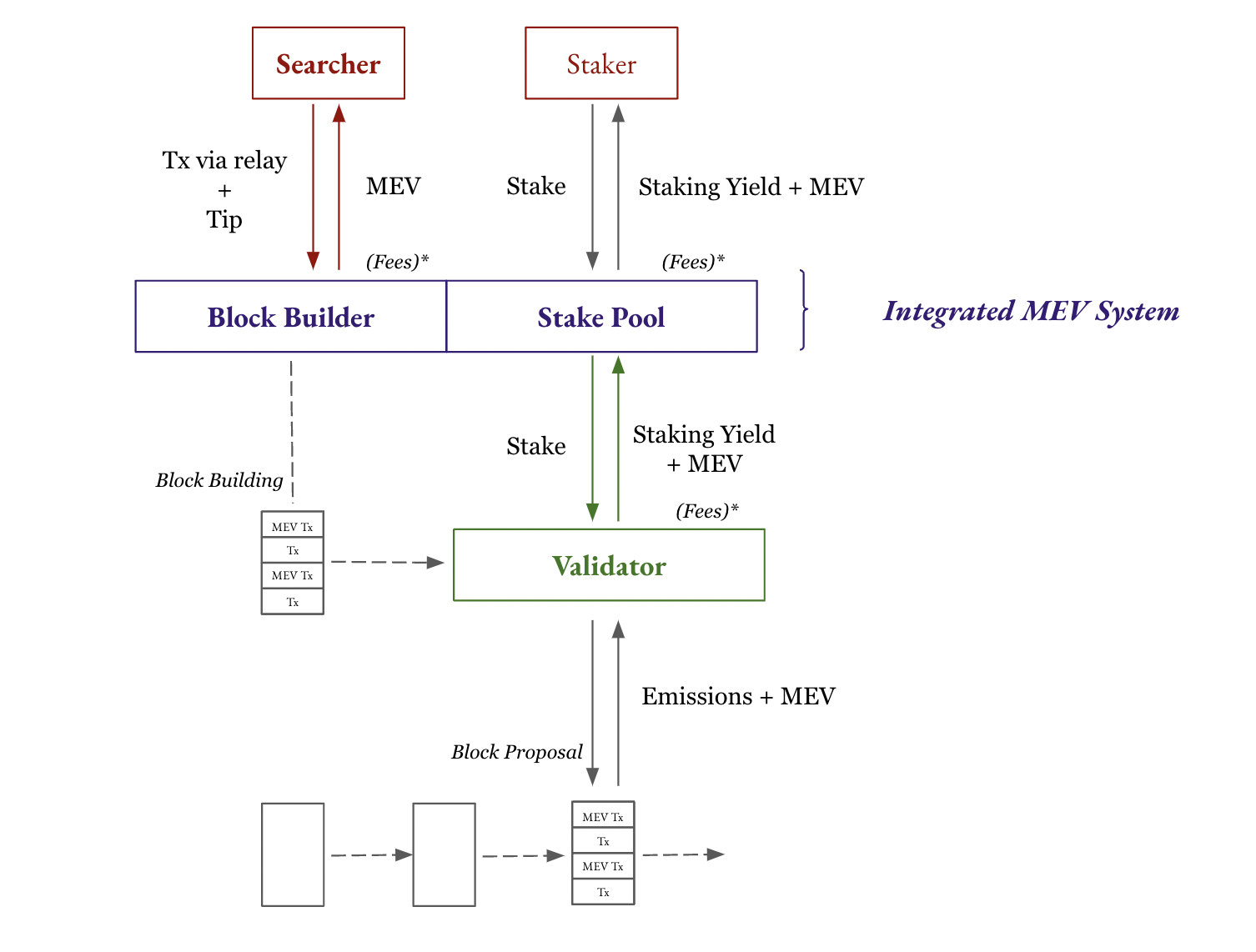

In proof-of-stake (PoS) systems however, the market structure for MEV is entirely different for two key reasons. First, stake pools participating in consensus allow for the redistribution of profits generated from searcher activity to the coalition of individual stakers. Second, the role of the miner is naturally separated into two distinct roles: validator (or block proposer) and block builder.

Integrated vs. Modular MEV Infrastructure

In PoS networks, there are four important actors in MEV:

- Stake pools — Stake pools aggregate L1 tokens from individual stakers and delegate them to validators participating in block production (e.g., Lido, Jito, Marinade, Coinbase Stake Pools)

- Searchers — Bots or individuals that identify and attempt to capture on-chain profit opportunities (e.g. transaction signers on Solana and Ethereum dashboards)

- Block builders — Entities that structure and sequence the transactions within a block (e.g., Jito Block Engine, Flashbots MEV-Boost)

- Validators (block proposers) — Validators or full nodes that vote with their stake in consensus to propose a block for validation by other nodes in the network. Services such as Staked, Figment, Chorus One, Staking Facilities run block proposers.

The central point of leverage in this ecosystem of actors is the stake pool (or more precisely, the individual staker that comprises the coalition), because stake ultimately grants validators the right to produce blocks. Validators need stake to maximize revenue, and the market for aggregating stake is competitive.

In order for stake pools to effectively aggregate stake, they must offer a competitive rewards rate to stakers. Historically, staking yields were fixed as a function of protocol emissions, and validators would compete on fees. Today, the amount of on-chain activity has increased, and the opportunity for differentiation among stake pools has as well. There are a few major ways that stake pools can now compete:

- Base emissions from producing blocks

- Fees or lack thereof

- Share of the MEV extracted

In order for stake pools to offer a competitive rewards rate, stake pools must delegate to validators that are building the most profitable blocks and ensure that those profits are shared back to their stakers. If validators are either inefficient at extracting MEV or choose to keep the MEV they extract for themselves, stake pools will swiftly re-allocate their stake elsewhere.

Searchers are constantly looking for opportunities on-chain or interfacing with decentralized order flow markets (e.g., DFLow). When searchers find a MEV opportunity that they want to win, they use relays supported by the block builder to submit their thoughtfully optimized transactions. They also include a tip for the validator (a fraction of the expected profit), which improves their rate of success. In a world where stake pools have the most leverage, those tips must be shared at least in part back to the stake pools so they can distribute competitive rewards to stakers.

Therefore, stake pools effectively mandate that validators source blocks from the most efficient block builders to maximize revenue for the stakers that comprise the stake pool. Block builders are also incentivised to build the most profitable blocks because they want more validators to include their blocks, which increases their success rate and potentially their percentage of MEV earnings.

The most dominant stake pools in proof-of-stake networks offer liquid staking derivatives (e.g., Jito’s jitoSOL, Lido’s stETH, Coinbase’s cbETH), which are tokens that represent a 1:1 claim on the original staked asset and accrue all staking rewards. The motivation for staking derivatives is to increase both capital efficiency and stake distribution.

Until recently, these ecosystem actors have all worked in concert as modular MEV infrastructure providers. However, as the opportunity for MEV capture grows, we expect MEV infrastructure to consolidate in an effort to improve value capture at every touch point in the value chain.

(Fees): This actor extracts fees from the one above it

Jito Labs is building the first full instantiation of this on Solana. We invested in them in August 2021, and today the Jito foundation launched stake pools, making their MEV infrastructure the first system with an integrated block builder and stake pool. They have also open sourced their own validator client (Jito-Solana) to more easily allow validators to participate in the system.

The Jito Block Engine enables off-chain blockspace auctions, and the Jito Stake Pool and liquid staking derivative (JITO-SOL) creates an integrated system that improves efficiency and therefore rewards to stakers.

MEV Value Accrual

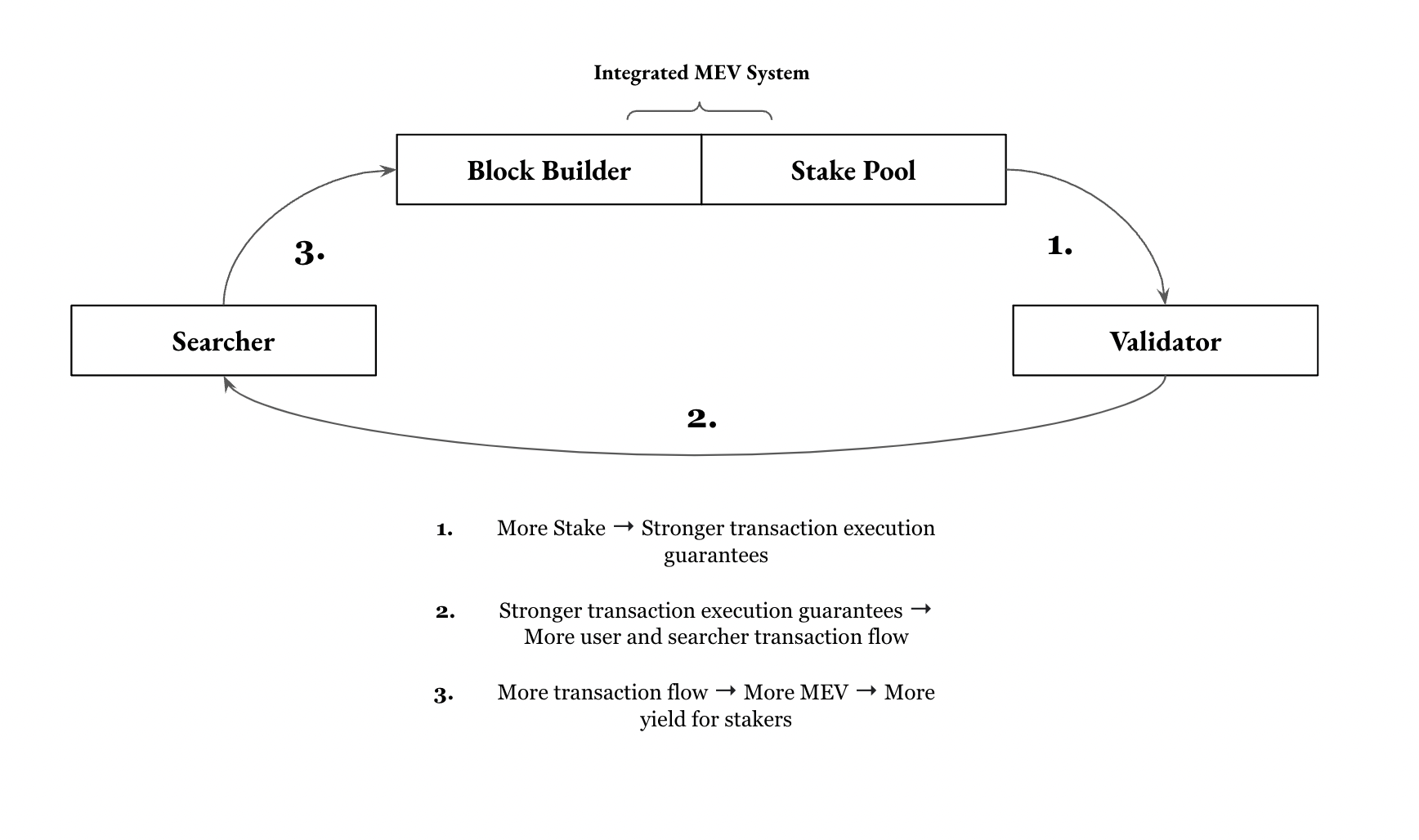

The market structure for MEV in proof-of-stake systems suggests that value will accrue at two layers: first with stakers via stake pools, and second with infrastructure providers that facilitate the extraction and redistribution of MEV. The more tightly integrated each component of MEV infrastructure is, the more effective the system will be at value capture.

In Protocols Don’t Capture Value, DAOs Manage Risk, we argued that statefulness and risk-management are necessary to drive sustainable value to any protocol. Integrated MEV systems manage risk across each layer of intermediation between searcher, stake pool, validator, and block builder.

For stakers, they manage risk by offering higher than market staking rewards rates. For searchers, by offering high probability transaction confirmation. For validators, by offering incremental revenues for block proposal via stake delegation. For block builders, by offering incremental revenues via higher probability of block inclusion.

Integrated MEV systems improve conditions for all actors in the value-chain. They present a considerably stronger position than any one modular actor in the system, and can therefore drive considerable returns to scale.

Disclosure: Unless otherwise indicated, the views expressed in this post are solely those of the author(s) in their individual capacity and are not the views of Multicoin Capital Management, LLC or its affiliates (together with its affiliates, “Multicoin”). Certain information contained herein may have been obtained from third-party sources, including from portfolio companies of funds managed by Multicoin. Multicoin believes that the information provided is reliable but has not independently verified the non-material information and makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in this blog are subject to change without notice and may differ or be contrary to opinions expressed by others.

The content is provided for informational purposes only, and should not be relied upon as the basis for an investment decision, and is not, and should not be assumed to be, complete. The contents herein are not to be construed as legal, business, or tax advice. You should consult your own advisors for those matters. References to any securities or digital assets are for illustrative purposes only, and do not constitute an investment recommendation or offer to provide investment advisory services. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by Multicoin, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by Multicoin is available here: https://multicoin.capital/portfolio/. Excluded from this list are investments that have not yet been announced (1) for strategic reasons (e.g., undisclosed positions in publicly traded digital assets) or (2) due to coordination with the development team or issuer on the timing and nature of public disclosure.

This blog does not constitute investment advice or an offer to sell or a solicitation of an offer to purchase any limited partner interests in any investment vehicle managed by Multicoin. An offer or solicitation of an investment in any Multicoin investment vehicle will only be made pursuant to an offering memorandum, limited partnership agreement and subscription documents, and only the information in such documents should be relied upon when making a decision to invest.

Past performance does not guarantee future results. There can be no guarantee that any Multicoin investment vehicle’s investment objectives will be achieved, and the investment results may vary substantially from year to year or even from month to month. As a result, an investor could lose all or a substantial amount of its investment. Investments or products referenced in this blog may not be suitable for you or any other party.

Multicoin has established, maintains and enforces written policies and procedures reasonably designed to identify and effectively manage conflicts of interest related to its investment activities. For more important disclosures, please see the Disclosures and Terms of Use available at https://multicoin.capital/disclosures and https://multicoin.capital/terms.

All Comments