Last week a U.S district court released its ruling for a landmark case in web3: The SEC vs LBRY Inc. The judge ruled in favor of the SEC, that $LBC, LBRY Inc.’s token, was an unregistered security, and in short: web3 lost a court case.

But before you give into the FUD and fear, let’s take a look into the actual case, what was charged, how LBRY acted and most importantly — what we can learn going forward.

You can read the full 22 page court ruling summary here.

Background

What is LBRY?

LBRY launched way back in 2016 as a blockchain for content hosting: “the first decentralized, open-source, fully encrypted content distribution service” (remember the 2016 specialized blockchains mania? Or was that 2022…?🤔).

The LBRY Network was supposed to be built of three things: the LBRY blockchain, the LBRY Data network and applications. LBC is the native token of the LBRY network, which launched in June 2016.

What was the SEC’s case?

The SEC filed the case in March 2021 (5 years later, really guys?) and claimed that LBS is an unregistered securities offering which violates section 5(a) & 5(c) of the Securities Act: unregistered offering of a security. Basically — LBC was never registered as a security with the SEC and LBRY has been selling it, thus an unregistered security offering.

To win, the SEC had to prove that LBRY Inc offered a security that wasn’t registered. The case relies on proving that LBC is a security.

The discussion now goes to the infamous Howey case and how securities are judged:

The Howey test is judged based on three criteria:

- The investment of money

- In a common enterprise

- With an expectation of profits to be derived solely from the efforts of the promoter or a third party

In the case against LBRY Inc, only the third point is in contention. LBRY Inc is clearly a common enterprise (they’re incorporated) and there was clearly an investment of money in via LBC. To prove that LBC is a security, the SEC has to prove the third clause for LBC to fail the Howey test.

The key question of the SEC case

Did potential investors think they would benefit from the work of the LBRY team? Thus constituting the third clause of Howey?

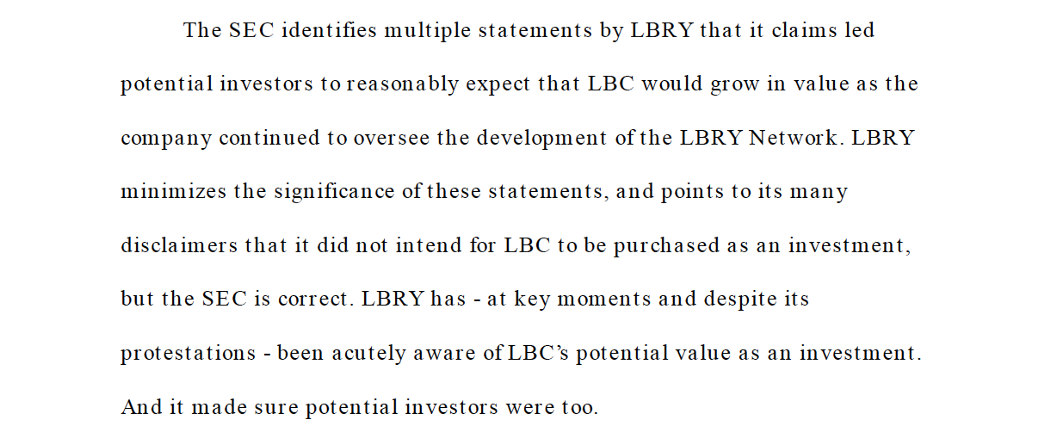

The SEC claimed yes, the LBRY team said no — and pointed to the many disclaimers they had regarding this, the utility of the LBC token and the fact that some users testified to purchasing LBC to use in the LBRY network and not as an investment.

The judge though, ruled says yes:

“LBRY has — at key moments and despite its protestations — been acutely aware of LBC’s potential value as an investment. And it made sure potential investors were too”

What did the Judge find problematic in LBC?

The judge based his decision that LBC was an investment contract with the expectation of profit from the efforts of others (the LBRY team) based on a three things:

- Network utility

- LBRY’s messaging

- LBRY’s business model

LBRY’s messaging

LBRY launched LBC early on, before the network had any real utility. It was a content network with only three pieces of content. The valuation ballooned due to speculation. In response the LBRY team made a few statements in blog posts that:

- They need to focus on building to bring the network to life

- They are aligned with the holders of the LBC token.

This is a clear indication that in order to bring value to the network and LBC tokens, the team needs to focus and work. LBC holders are reliant on this — the efforts of the team.

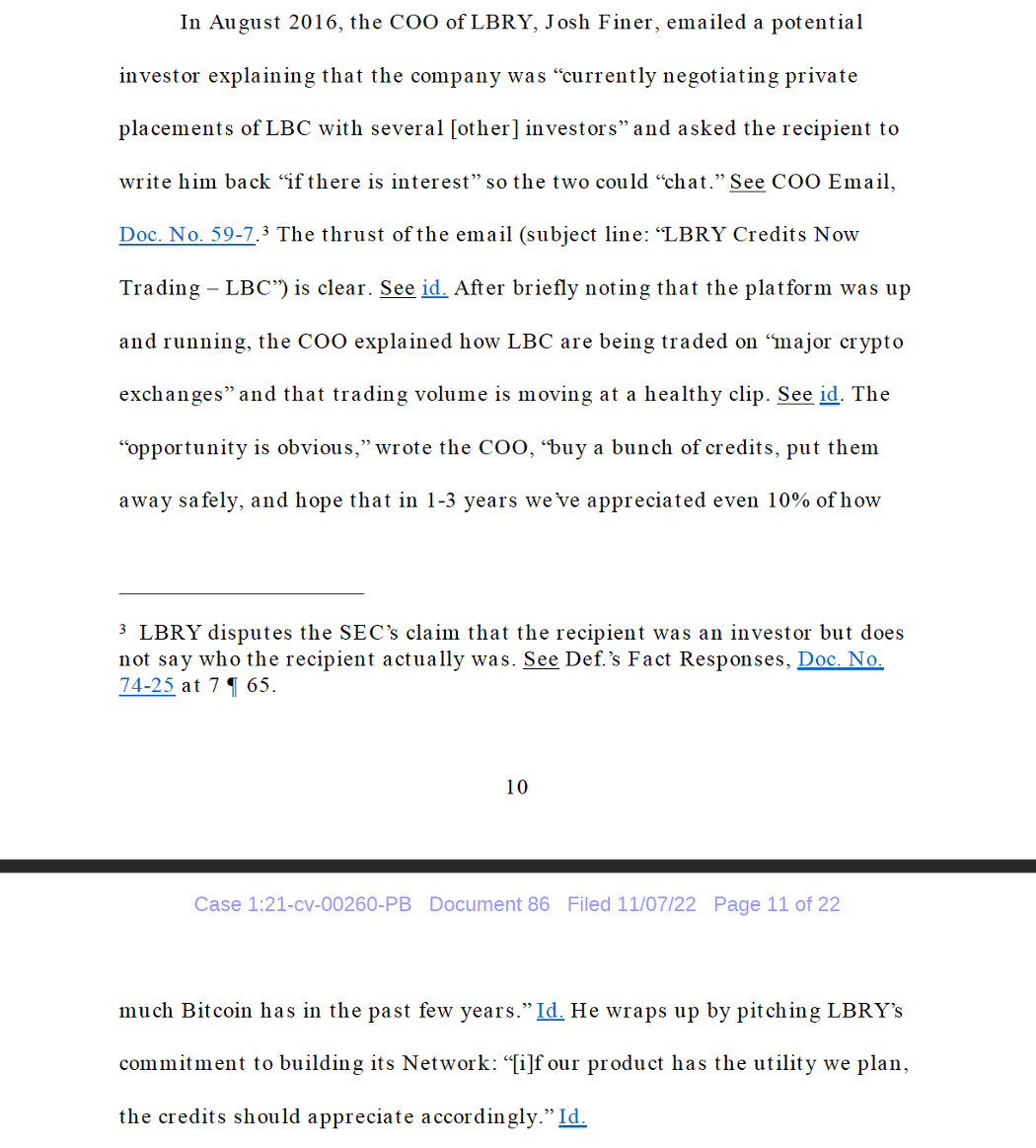

Beyond public blog posts, The LBRY team marketed LBC privately as an investment to investors. Internal emails show black on white that it’s an investment opportunity based on their teams’ future work.

The LBRY team communicated along the way that they’re hard at work creating a network that will increase the value of LBC.

Messaging takeaways

- When you launch with no utility it’s clear that the team needs to build out the network and thus token holders have an expectation of profit from the efforts of others (i.e the team). If you’re launching with sufficient utility built out, this could be less clear that the token value is reliant to a sufficient degree upon the efforts of the team.

- Beware how you communicate! Internally and externally (the court also brings a Reddit post as evidence — today Discord could be utilized as well). If you treat your token like a security, so will the courts.

- Disclaimers don’t mitigate economic realities:

LBRY’s business model

The judge deemed that LBRY’s business model was solely reliant on the growth in value of LBC. There was no other way for them to redeem their time and money investment.

This was based on the Network Whitepaper and token distribution. 10% of LBC was allocated to the team and founders. This was their only profit, hence they needed the token to rise in price and would want to work diligently to promote it.

More so, out of a one billion created tokens, a pre mine of 400 million LBC was ear marked for the LBRY team. The distribution should look similar to many current projects: 200 million for a community fund, 100 million to an institutional fund and 100 million for operations — the 10% for paying the team. Most of the rest would go to miners.

The judge deemed that this structure would lead any reasonable investor to assume that they would benefit from LBRY’s work on the protocol — as the LBRY team held 40% of the total allocation in a pre-mine and was thus heavily incentivized to work on the protocol.

The nail in the coffin is this statement (pg. 17):

“Simply put, by intertwining LBRY’s financial fate with the commercial success of LBC, LBRY made it obvious to its investors that it would work diligently to develop the Network so that LBC would increase in value”

Simply, this statement is a bullet in the heart of aligning interests between a company and its token holders. It rules that this alignment of interest, which is at the crux of many web3 companies is a sign of failing the Howey Test.

Business model takeaways

- Token holders can’t reasonably expect the token value to go up because of the company’s effort. This means that tokens need to be more widely distributed among holders so that token holders don’t assume this.

- The company’s success can’t be tied up only in the success of the token. An alternative business model can help prove that the token isn’t the core of their work and thus token holders shouldn’t hope to benefit from their effort.

Network utility

What about utility? LBC was a utility token to use the LBRY network. Some people purchased it for utility and that is its primary use case in the network protocol.

But the judge, like Joey, ruled otherwise.

In an important statement the judge claims that LBRY is mistaken both about the facts and the law.

- No law stipulates that a utility token can’t also be an investment contract.

- The fact that some users purchased it for utility doesn’t mean that LBRY didn’t offer it as a security.

Utility takeaways

- Having a utility token doesn’t mean it’s not ALSO an investment contract.

- The offering and the messaging is what matters, not how the token is used.

Summary of the LBRY case

LBRY offered the LBC token as an investment contract where holders could expect to benefit from the effort of others — the LBRY team. It’s clear from their marketing and communication, both internally and externally as well as the way the network was launched — with no real utility and a business model that relies entirely on LBC growing in value. Utility for the token or for some purchasers doesn’t negate this.

Messaging around tokens is now trickier than ever. Talking about price movements and building is now a red flag in the eyes of the law. Importantly, the key premise of using a token to align incentives came under review. To reiterate this point from pg. 17:

“Simply put, by intertwining LBRY’s financial fate with the commercial success of LBC, LBRY made it obvious to its investors that it would work diligently to develop the Network so that LBC would increase in value”

That’s part of the key promise of web3. This ruling shows the trickiness in linking a token to a company where token holders can legitimately expect to benefit from the hard work of the company.

However, it’s not as clear cut how this ruling applies to decentralized protocols where there is no team who is hard at work and thus token holders don’t necessarily have that same expectation. In many cases a token promoted by a single company IS a security — that’s what a share is at the end of the day — an alignment mechanism between management and shareholders. This is not necessarily the case for decentralized protocols.

All Comments