What is cost basis in crypto?

In the context of cryptocurrencies, “cost basis” refers to the initial outlay paid for digital assets. It is an important consideration when calculating capital gains or losses from the sale or disposal of cryptocurrencies. The capital gains or losses on an investor’s crypto sale are calculated as the selling price minus the cost basis.

To avoid tax complications, the cost basis must be reported accurately; otherwise, one may have an underpayment or overpayment of taxes, which may result in fines from the tax authorities. Furthermore, accurate reporting is much more important due to the increased scrutiny that tax authorities throughout the world are placing on crypto transactions.

Tax authorities require individuals to declare their cryptocurrency transactions for tax purposes in numerous jurisdictions, including the United States. Penalties and audits may result from inaccurate cost basis reporting. As a result, investors must keep thorough records of all of their cryptocurrency transactions, including the purchase price, the date of the transaction and any additional costs.

Common methods for calculating crypto cost basis

There are various methods to calculate the cost basis for cryptocurrencies, as discussed below:

Specific identification

Specific identification is a popular method for calculating the cost basis of cryptocurrency holdings. Investors are able to determine and monitor the cost basis of each cryptocurrency asset separately using this method. Investors who are selling or disposing of crypto assets indicate the exact units they are selling and the price at which they were purchased.

Because this method accounts for the specific purchase price of the units being sold, it enables an accurate cost basis calculation. It is especially helpful for investors who wish to carefully choose what units to sell depending on their cost basis and holding duration to optimize their tax outcomes.

To understand how this method works, let’s consider a hypothetical example: An investor purchased 1 Bitcoin on Jan. 1, 2023, for $30,000 and 1 BTC on May 1, 2023, for $50,000. They can select which particular purchase to utilize as their cost basis if they choose to sell 1 BTC.

To implement a specific identification method, every crypto transaction must be meticulously documented, including the purchase price, date and any associated costs. Compared to other approaches, it may also be more difficult and time-consuming to execute, even if it provides the highest level of accuracy in cost basis reporting.

First-in, first-out (FIFO)

Another common way to calculate the cost basis of crypto holdings is the “first-in, first-out” (FIFO) method. Under FIFO, the crypto assets that are bought first will be sold first. This approach assumes that the oldest cryptocurrency holdings are the ones being sold or otherwise disposed of, which makes transaction tracking easier.

Let’s assume that on Jan. 1, 2023, an investor paid $30,000 to acquire 1 BTC; on May 1, 2023, they paid $50,000. The oldest purchase price — i.e., $30,000 — is automatically used as the cost basis when they sell 1 BTC.

Even though FIFO is simple to implement, there are situations in which it may result in increased tax costs due to the possibility that assets with lower purchase prices would be sold, increasing capital gains and, in turn, taxes.

Despite this drawback, FIFO remains a popular option for many investors because it is straightforward to apply; people who are not actively trading cryptocurrencies prefer such a method for calculating their tax liabilities.

Last-in, first-out (LIFO)

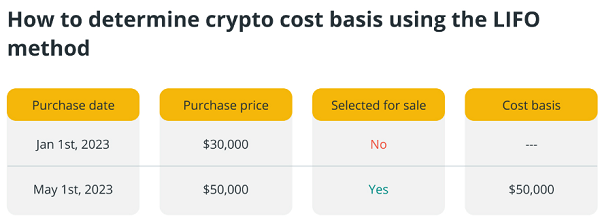

As opposed to FIFO, “last-in, first-out” (LIFO) assumes the crypto assets that were most recently bought will be sold first, indicating that the most recent purchase price serves as the asset’s cost basis.

Let’s assume that on Jan. 1, 2023, an investor paid $30,000 to acquire 1 BTC, and on May 1, 2023, they paid $50,000. When they sell 1 BTC, the cost basis is automatically the most recent purchase price.

In some circumstances, the LIFO approach may be beneficial, particularly when prices are rising. Investors may be able to reduce their capital gains and, in turn, their tax obligations by selling their most recent acquisitions first. However, in cases where the most recent assets acquired have a lower cost basis than older assets, LIFO can also result in greater taxes.

Compared to FIFO, the LIFO approach is less frequently employed to determine crypto tax liabilities despite possible tax benefits. This is because LIFO may be less desirable to many investors due to its potential complexity and the need for more thorough record-keeping.

Highest-in, first-out (HIFO)

A strategic way for determining the cost basis of crypto holdings for taxation purposes, the “highest-in, first-out” (HIFO) method assumes that the most expensive cryptocurrency assets are sold first (in contrast to FIFO and LIFO).

Investors can strategically reduce their capital gains and, thereby, their tax liability by selling their assets on the highest-cost basis first. When there is a price appreciation and the cost basis of the assets being sold is higher, this strategy is especially advantageous.

To understand how the HIFO method works, let’s assume that an investor purchased 1 BTC on Jan. 1, 2023, for $30,000, followed by 1 BTC on May 1, 2023, for $50,000. When they sell 1 BTC, the cost basis is automatically the highest purchase price.

Although HIFO can lead to lower capital gains taxes, it may not be a good fit for all investors, as it requires careful record-keeping. Additionally, investors should ensure they keep proper documents to back up their calculations because tax authorities may scrutinize the use of HIFO. Notwithstanding these drawbacks, investors wishing to reduce their tax obligations on crypto transactions may utilize the HIFO approach.

Average cost basis (ACB)

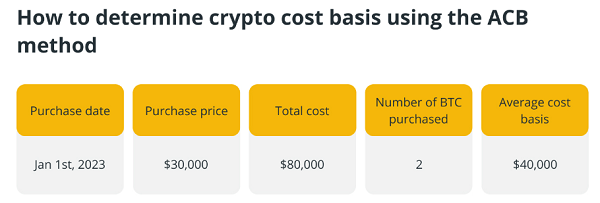

By using this technique, investors may calculate the average price of all the cryptocurrencies they own. The cost basis of the sold crypto assets is then established using this average price.

Let’s assume an investor purchased 2 BTC, 1 at $30,000 (Jan. 1, 2023) and 1 at $50,000 (May 1, 2023). Their average cost basis would be calculated as follows:

The average cost approach offers a middle ground between potential tax optimization and simplicity. Adopting an average price for all holdings of the same cryptocurrency makes calculating the cost base simpler. Investors who frequently buy and sell cryptocurrencies and wish to expedite their record-keeping procedures may find this strategy helpful.

The average cost approach is still a popular choice among investors despite perhaps not providing the same level of tax efficiency as FIFO or HIFO, for example. While still providing a reasonable degree of accuracy in cost basis reporting, it also aids in ensuring compliance with tax requirements.

Documentation required for accurate cost basis calculation

In the case of cryptocurrencies, complete transaction documentation is necessary for an accurate cost basis assessment. Investors need to maintain thorough records of the following data:

Date and time of purchase: The date and time when cryptocurrency was purchased.

Purchase price: The cost incurred when purchasing a cryptocurrency.

Transaction fees: Any costs — e.g., gas fees — incurred while making a purchase.

Type of transaction: Whether it was a purchase, sale, exchange or another type of transaction.

Wallet addresses: The addresses involved in the transaction.

Transaction ID: A unique identifier assigned to every transaction.

Documentation is essential for tax reporting purposes to ensure compliance with tax legislation and reduce the possibility of errors or discrepancies in capital gains calculations. Furthermore, thorough record-keeping might assist investors in properly responding to any tax authorities’ audits or queries.

Variations in crypto cost basis calculation among different jurisdictions

Different countries use different methods to determine the cost basis of cryptocurrencies, which affects investors’ tax liabilities. The “pooled” strategy, an adaptation of the ACB method, is the most widely used technique in the United Kingdom. Using this strategy, investors calculate the average cost of all identical cryptocurrency holdings to determine the cost basis for tax purposes.

The specific identification approach is commonly utilized in Canada to facilitate tax optimization. The United States permits specific identification but leans toward FIFO as the default method.

A few methods are used in Australia, such as specific identification, FIFO and, in some cases, ACB. It’s important to remember that certain tax regulations can change, and seeking professional advice tailored to your jurisdiction is always the safest approach.

Calculating cost basis for different types of crypto transactions

Calculating the cost basis for different types of cryptocurrency transactions requires specific considerations:

Buying cryptocurrency

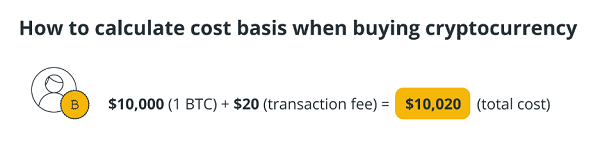

The sum of money spent on purchasing a cryptocurrency serves as its cost basis. This covers the cost of the cryptocurrency and any transaction fees paid at the time of purchase.

Example: The total cost basis would be $10,020 if an investor paid $10,000 for 1 BTC and a $20 transaction fee.

Selling cryptocurrency

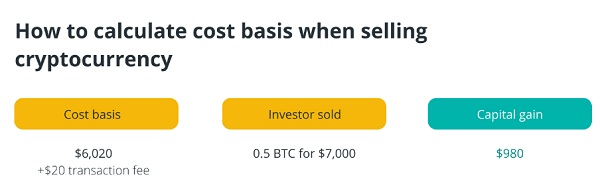

The capital gains or losses on a cryptocurrency sale are calculated by deducting the cost basis from the selling price. The initial cryptocurrency purchase price plus any transaction fees paid at the time of purchase make up the cost basis.

Example: The capital gain would be $980 if an investor sold 0.5 BTC for $7,000 and its cost basis was $6,020 (plus a $20 transaction fee).

Exchanging cryptocurrency for goods or services

The fair market value of the cryptocurrency at the time of the exchange serves as the cost basis for trading it for goods or services. It is determined by the value of the cryptocurrency in U.S. dollars at the time of the transaction.

Example: The cost basis for the transaction would be $700 if an investor traded 0.1 BTC for a $500 product, and the fair market value of 0.1 Bitcoin at the time of the exchange was $700.

Receiving cryptocurrency as income or gifts

The fair market value of a cryptocurrency at the time of receipt serves as the cost basis for receiving cryptocurrency as gifts or income. Usually, the value of the cryptocurrency in U.S. dollars at the time of receipt determines this amount.

Example: If an investor receives 0.2 BTC as a gift and its fair market worth is $1,300, then $1,300 would be the cost basis of the gifted Bitcoin.

How to handle various crypto events for cost basis calculation

Hard forks and airdrops

The cost basis of new cryptocurrency obtained via hard forks and airdrops is typically regarded as $0. However, since it will be used to determine capital gains or losses when the new cryptocurrency is subsequently sold or otherwise disposed of, it is crucial to keep track of the fair market value of the cryptocurrency at the time of receipt.

Example: If a hard fork or airdrop results in an investor receiving five units of a new cryptocurrency and each unit’s fair market value is $100 at the time of receipt, then $500 would be the new cryptocurrency’s cost basis.

Staking and mining rewards

Rewards for staking and mining are normally recognized as income at the cryptocurrency’s fair market value on the date of receipt. The fair market value becomes the cost basis for the cryptocurrency received.

Example: The cost basis for the staked cryptocurrency would be $200 if an investor received five units of the cryptocurrency as a staking reward, and the fair market value of each unit at the time of receipt was $40.

Crypto-to-crypto swaps

The fair market value of the cryptocurrency given up at the time of the swap is used to determine the cost basis of the new cryptocurrency acquired via a crypto-to-crypto swap. This fair market value serves as the new cryptocurrency’s cost basis.

Example: If an investor swaps 2 BTC for 100 units of a different cryptocurrency and the fair market value of 2 BTC at the time of the swap is $150,000, the cost basis for the new cryptocurrency would be $150,000.

Adjusting crypto cost basis for transaction fees and other costs

The cost basis of cryptocurrency assets must be adjusted for transaction fees and other associated expenses. One way to do this is to include transaction costs in the cost basis. When buying a cryptocurrency, for example, the total cost basis should include any fees paid during the transaction in addition to the asset’s purchase price. Similarly, all transaction fees related to the sale of a cryptocurrency should be deducted from the revenues.

Investors should also take exchange fees and other expenses into account in addition to transaction fees. It is important to include these fees — which cryptocurrency exchanges charge for executing trades — in the total cost basis calculation. Investors can ensure that their cost basis calculations appropriately reflect the total amount invested in purchasing and disposing of crypto assets by accounting for transaction fees and other associated expenses.

Benefits of using crypto tax software for accurate tax filings

For correct tax reporting, there are a number of advantages to using crypto tax software. Firstly, it saves investors’ time and lowers the possibility of mistakes in their tax filings by automating the process of calculating capital gains and losses. These platforms can easily integrate with wallets and cryptocurrency exchanges, importing transaction data automatically and producing comprehensive reports for tax purposes.

Secondly, by using the proper cost basis technique and taking transaction fees and other expenses into account, crypto tax software ensures that tax requirements are followed. By doing this, investors can reduce the possibility of audits or fines from tax authorities by appropriately disclosing their cryptocurrency transactions.

These platforms also offer real-time tax estimations, which allow investors to evaluate their annual tax obligations and make well-informed decisions regarding their cryptocurrency holdings. Furthermore, many cryptocurrency tax software solutions provide tax-loss harvesting capabilities, which enable investors to optimize their tax outcomes by deliberately offsetting gains with asset sales.

All Comments